Why Market Downturns Are Our Friend!

A young colleague of mine was shocked when she looked at her most recent 401K investment returns. You see, her relatively short experience with investing has been contained entirely during the longest bull market in modern history. For someone who’s entire experience was during this period, the idea that we could lose money by saving seemed foreign. I was being asked all kind of questions and she was honestly thinking of getting out of the market and putting all of her money in the bank! In the coming months we will be hearing a lot of folks talking about doing just that.

Downturns don’t matter to long-term investors

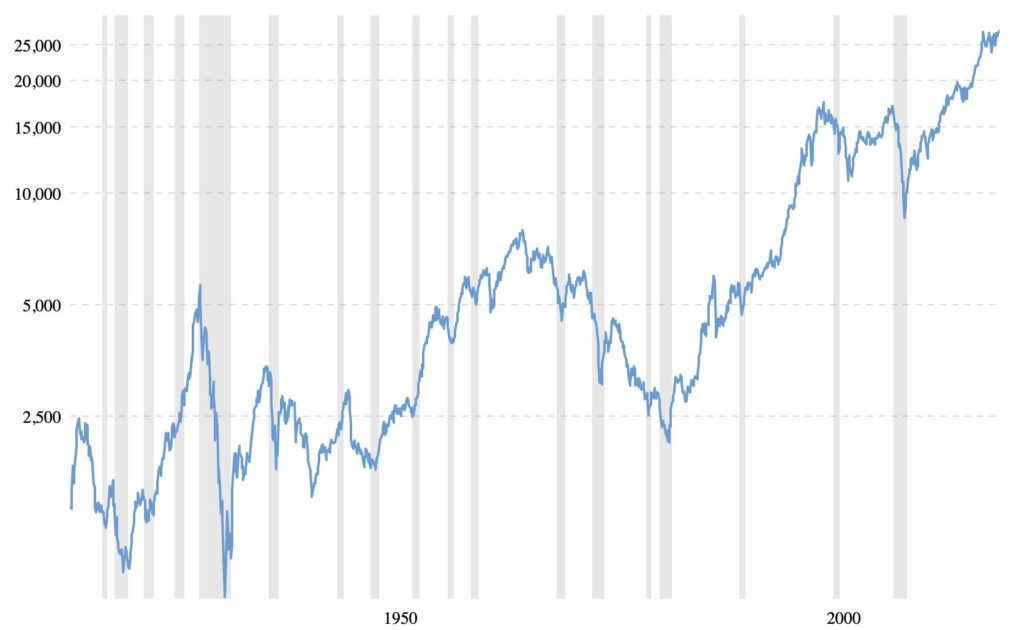

According to one source, the average American has ~ $100,000 saved for retirement. This isn’t nearly enough – but that’s a discussion for another time. If we look at the DJIA at the peak of the bull market, Sept 21, 2018 (26743), and compare it to Dec 12, 2018 (24593) we have a negative 8.0% return over the past 2 ½ months. The average American – on paper – could have lost $8,000 in 82 days. However, there are some important things to consider. First, you shouldn’t be fully invested in the stock market, so the loss on a balanced portfolio is probably much less than 8.0%. (Read about balanced portfolios here). Secondly, and this is critically important to remember, unless you absolutely need the money now, the loss is only on paper. Its meaningless. Only if you sell your investments does the loss becomes real. Let’s look at the DJIA over the past one hundred years.

(Microtrends.net)

If anything becomes apparent it’s that no matter how badly the market drops, historically it has always come back and each cycle goes higher. Past performance never guarantees future returns; however, even after the great depression, stocks continued to hit new highs. For those that could wait it out, they eventually recovered their money and made more. Those that sold their shares were wiped out in the 81% drop in value that occurred from 1929 to 1932. Seems like common sense in 2018 where we have the advantage of hindsight as well as better regulatory agencies and safety nets – but in 1929 it would have seemed quite different.

Why bears are an investors friend!

So what should you do right now? Exactly what you have been doing – continue to invest in a balanced portfolio. The best part of a bear market is that it allows us to take advantage of dollar cost averaging. Dollar cost averaging is a simple strategy whereby we invest a fixed amount of money on a consistent schedule regardless of market performance. For example, let’s say that we invest $100 in a stock every month regardless of its price that month. The result is that we get more shares for our $100 when prices are low, and fewer shares when prices are higher. Iets see how this works in our favor during a bull market, let’s look at an imaginary stock called the DJIA. The stock starts the year off strong and then the price tanks in the middle of the year only to rally by December. I did mention this was an imaginary stock in an imaginary stock market didn’t I?

| Stock Price | # of shares | Total Invested | |

| Jan | 25 | 4.00 | 100 |

| Feb | 24.5 | 4.08 | 100 |

| March | 26 | 3.85 | 100 |

| April | 20 | 5.00 | 100 |

| May | 17 | 5.88 | 100 |

| June | 15 | 6.67 | 100 |

| July | 15 | 6.67 | 100 |

| Aug | 18 | 5.56 | 100 |

| Sept | 20 | 5.00 | 100 |

| Oct | 22 | 4.55 | 100 |

| Nov | 24 | 4.17 | 100 |

| Dec | 25 | 4.00 | 100 |

| 59.41 | 1200 |

So we invested $1,200 over the course of a year ($100 / month) and if the price had remained $25 a share all year we would have purchased 48 shares worth exactly $1,200. An average price of $25 a share. Nothing earned and noting lost. But the price dropped – there was a bear market that lasted just a few months. Every $100 invested earned us more than 4 shares. We ended up with 59.41 shares worth $1,485 – an average of $20.20 a share. We made $285 – on paper – by just sticking with our monthly investment strategy. If we stopped investing or sold our investments in June or July we would have totally missed this opportunity and potentially lost money.

This is exactly why a bear market is the best time to continue our disciplined investment strategy of investing every month. Making our normal periodic investments into 401Ks IRA and the like while everone else is selling is the easiest way to make money – in the long run. Moral of the story – Don’t fear the bear, feed the bear!

2 Comments

The Vetducator

I can’t WAIT for the next market correction! I will be so giddy- get stocks on sale! I understand I am in a privileged position as someone still drawing a salary and not living off their investments. But for all of us working stiffs, the next correction will be a great chance to snatch up some cheap stocks!

Pingback: